Germany offers some of the most generous parental leave policies in the world. Between Mutterschutz (maternity protection), Elternzeit (parental leave), and Elterngeld (parental allowance), you can spend up to three years raising your child without losing your job. But what happens to your health insurance during this time?

The answer depends entirely on whether you are publicly or privately insured, and whether you are a mandatory or voluntary member. Let's break it down.

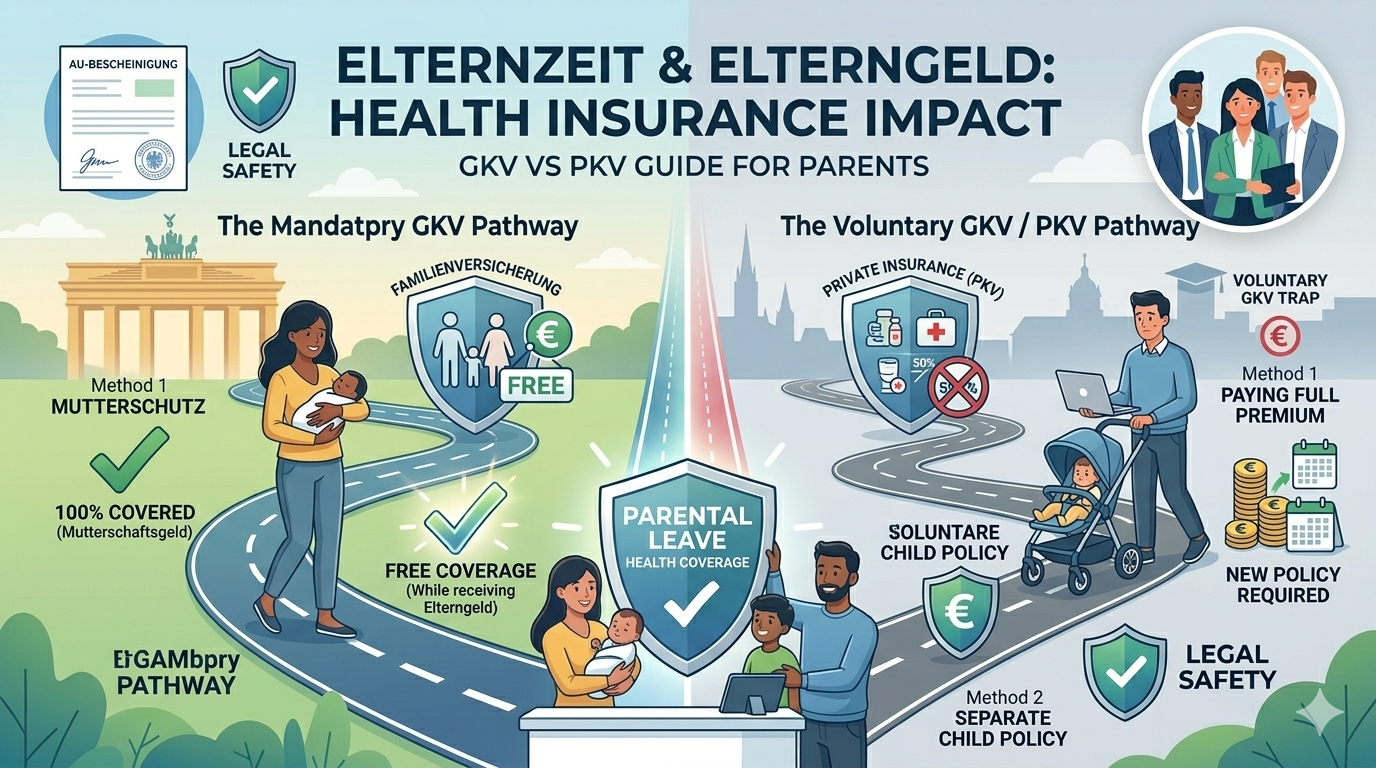

1. If You Have Public Insurance (GKV) - Mandatory Member

This is the most common and advantageous situation. If you are a standard employee earning less than the annual threshold (JAEG, roughly €77,400 in 2026), you are a "mandatory member" (pflichtversichert).

- During Mutterschutz (6 weeks before, 8 weeks after birth): You remain fully insured. You don't pay any premiums from your Mutterschaftsgeld (maternity pay).

- During Elternzeit: Good news! As long as you are receiving Elterngeld and are not working part-time, your public health insurance is completely free of charge. Your coverage continues uninterrupted.

2. If You Have Public Insurance (GKV) - Voluntary Member

If you are a high-earner (earning above the threshold) but chose to stay in the public system, or if you are a freelancer, you are considered a "voluntary member" (freiwillig versichert).

- The Trap: Unlike mandatory members, voluntary members do not get free insurance during Elternzeit by default. You will have to pay the minimum monthly contribution (around 220€ - 240€) out of your own pocket.

- The Exception (Family Insurance): If you are married to someone who is a mandatory member of the public health insurance system, you can switch to their Familienversicherung (family insurance) during your Elternzeit. This makes your insurance free!

3. If You Have Private Insurance (PKV)

Private insurance operates on contracts, not solidarity. Therefore, there is no "free" period during parental leave.

- You Must Keep Paying: You have to continue paying your full private insurance premium during Mutterschutz and Elternzeit. This can take a massive chunk out of your Elterngeld (which is capped at €1,800/month).

- Your Employer Stops Paying: Normally, your employer pays ~50% of your private premium. During Elternzeit, this employer contribution stops completely. You must pay 100% of the premium yourself.

- The Child Needs a Separate Policy: Unlike public insurance, your newborn is not insured for free. You must buy a separate private policy for them (which costs roughly 150€ - 250€ per month).

4. Working Part-Time During Elternzeit

If you decide to work part-time during your parental leave (up to 32 hours per week allowed), your insurance status goes back to normal. Your part-time salary will be assessed, and health insurance contributions will be deducted from your paycheck just like a regular employee.

Action Steps Before the Baby Arrives

If you are privately insured or a voluntary public member, calculate how much your insurance will cost during Elternzeit. Set this money aside before the baby arrives, as your Elterngeld will be significantly reduced once insurance premiums are paid.