One of the most significant advantages of the German Statutory Public Health Insurance (GKV) system is its solidarity-based approach to family coverage. Unlike in many other countries, you don't always have to pay a separate premium for every member of your household.

The Familienversicherung (Family Insurance) allows you, as a publicly insured member, to include your spouse, registered civil partner, and children in your plan at no additional cost. This comprehensive guide will walk you through who is eligible, the requirements, and the step-by-step process to secure this free coverage for your family in Germany.

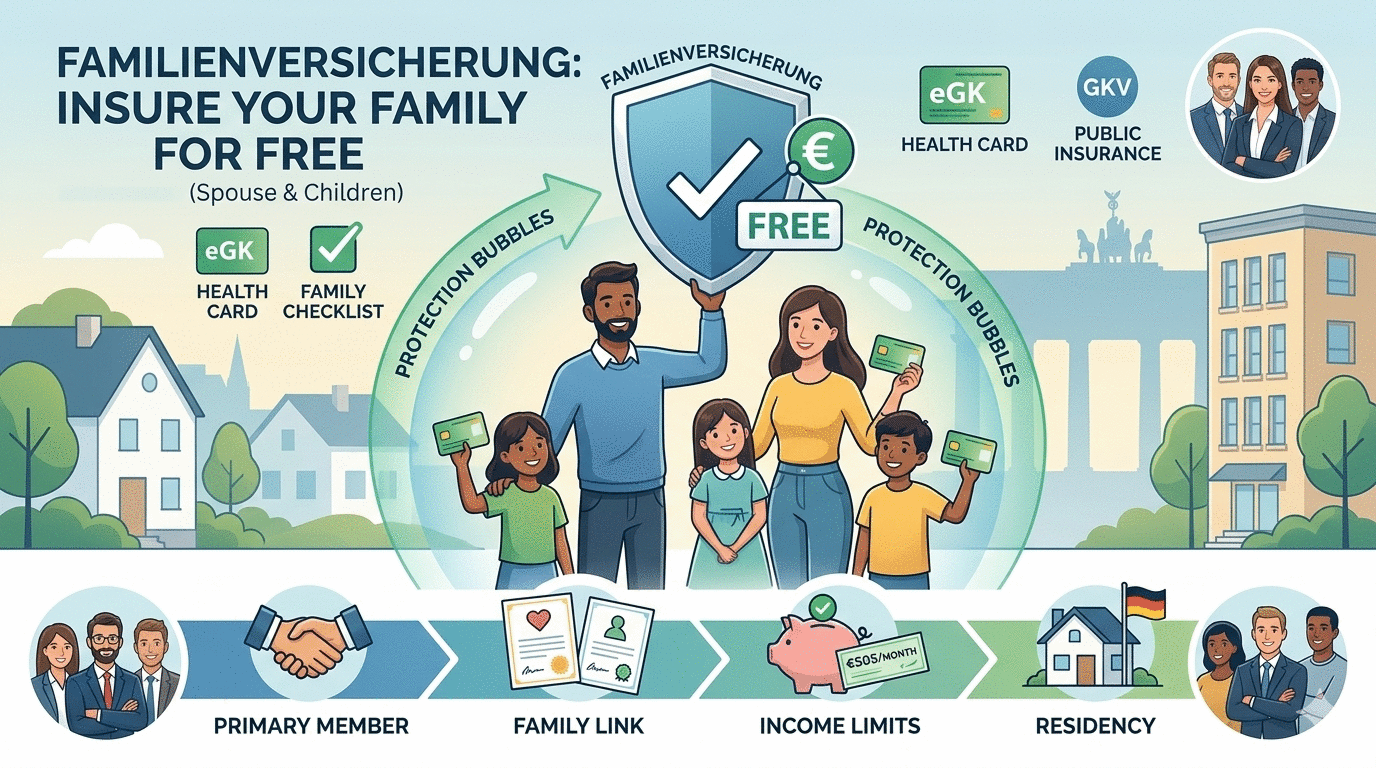

Part 1: Who is Eligible for Familienversicherung?

To benefit from the Familienversicherung, specific criteria must be met by both you (the primary insured member) and the family members you wish to include.

1. Requirements for You (The Primary Member):

- You must be a member of a Statutory Public Health Insurance provider (like TK, AOK, Barmer, etc.).

- Your insurance type must allow for family coverage. This includes most employees, pensioners, students, and publicly insured self-employed individuals (but typically not those in Private Health Insurance – PKV).

2. Requirements for Your Family Members (Spouse & Children):

- Family Link: They must be your legal spouse, your registered civil partner, or your biological/adopted children. Stepchildren and grandchildren can also be covered under specific conditions (e.g., if they live in your household and you provide for them).

- Income Limits (The Most Critical Step): This is the key requirement. Your family members must not have their own regular income that exceeds a specific threshold. For 2026, the generalized income limit is approximately €505 per month. This includes income from employment, rental properties, investments, and capital gains. If they have a "Mini-job" (earnings up to €538/month), they may still be eligible, but any higher employment income generally voids the free coverage.

- Own Insurance: They must not already have their own mandatory insurance (e.g., through their own job).

- Residency: They must legally reside in Germany.

Part 2: Special Considerations for Children

The rules for children have their own nuances, especially regarding age and education.

Age Limits:

- Up to 18: Children are covered up to their 18th birthday.

- Up to 23: Coverage continues if the child is unemployed.

- Up to 25: Coverage extends if the child is still in school or university. This includes vocational training (Ausbildung), provided their vocational training salary doesn't make them obligatorily insured themselves.

- Unlimited: For children with disabilities who cannot support themselves.

The Private Insurance (PKV) Caveat

A very common and critical situation arises when one parent is Privately Insured (PKV) and the other is Publicly Insured (GKV). If the PKV parent has a higher income that exceeds the statutory cap (Beitragsbemessungsgrenze), the children might not be eligible for free GKV family insurance. Instead, they must be privately insured with the PKV parent. It is crucial to check with your insurance providers to clarify this before assuming your children are covered for free.

Part 3: Step-by-Step Guide to Applying for Familienversicherung

Once you've confirmed eligibility, the process is straightforward:

- Contact Your Insurer: Reach out to your health insurance company (Krankenkasse). Most insurers (like TK or AOK) have dedicated English-speaking phone lines and easy-to-use online portals.

- Request the Form: Ask for the "Fragebogen zur Familienversicherung" (Family Insurance Questionnaire). This form collects details about your family members, their residency, and their income.

- Gather Documents: You will need to submit supporting documents. This typically includes:

- For Spouse: A translated (if necessary) marriage certificate.

- For Children: Birth certificates.

- For Students: An official enrollment certificate (Immatrikulationsbescheinigung) for children over 18.

- Proof of Income: Pay slips, tax assessments, or other documents proving your family member's income (or lack thereof).

- Submit the Form: Fill out the questionnaire accurately and submit it along with all required documents to your Krankenkasse.

- Receive Your Cards: Once processed and approved, your family members will receive their own electronic health insurance cards (eGK), giving them full access to the medical system.

Summary and Key Expat Advice

The Familienversicherung is a fantastic financial benefit of living and working in Germany, potentially saving you hundreds of euros per month. To make sure you get the most out of it:

- Be Proactive: Start the process as soon as your family arrives and registers in Germany.

- Be Honest About Income: Insurers regularly check income. Failing to declare changes can lead to having to pay back insurance premiums retroactively.

- Clarify PKV Scenarios: If one parent is private, always confirm eligibility directly with the insurers.