Germany is famous for its regulations, but some of the most critical ones are not laws; they are social norms. While not a single German law states, "You must buy private liability insurance," if you ask a local, they will tell you it's the first thing you must do.

For expats, the Haftpflichtversicherung is the most misunderstood "optional" insurance that, in reality, is virtually mandatory for a legal and safe life. Here is why failing to have one is the biggest risk you can take in Germany.

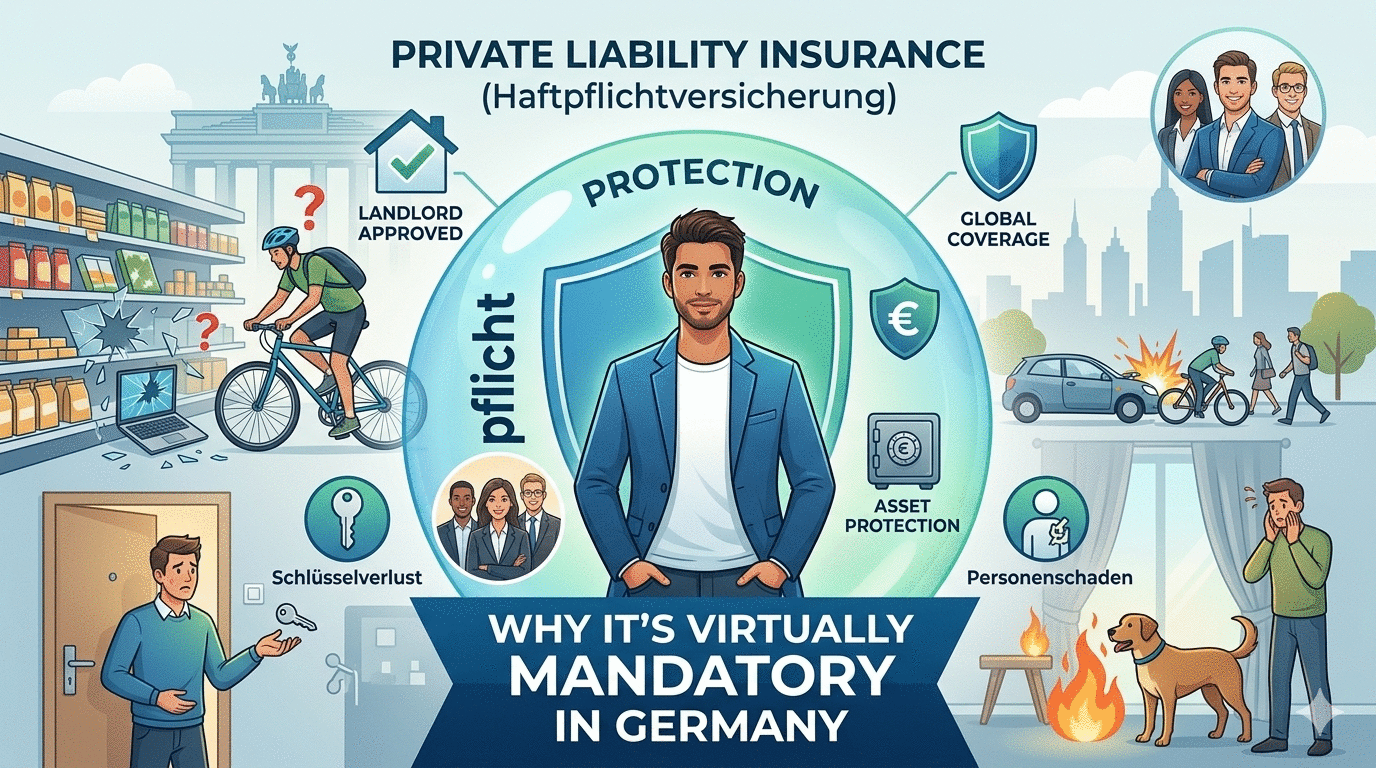

What is Private Liability Insurance?

In Germany, the legal principle of liability is straightforward: "If you accidentally damage someone else's property, you must pay to repair or replace it."

- The Problem: There is no financial limit to this liability. If you drop a coffee on a laptop, you pay a few hundred euros. But what if your actions cause a car accident, injure someone, or damage an historic building? You are liable with all your current and future assets.

Why is it Practically Mandatory?

There are two main reasons why every German has it, and every expat must too:

1. Landlord Requirement (The Key to Housing)

Due to Germany's difficult housing market, landlords have their pick of tenants. In 90% of cases, when you apply for an apartment, you must present a certificate from your Schufa (credit score) and proof of your Haftpflichtversicherung.

A landlord won't risk you accidentally burning down their apartment or damaging the structure unless they know an insurance company will cover the costs. Without it, you simply will not get a rental contract.

2. Lifelong Protection Against Accidents

Life happens. A simple, honest mistake can lead to catastrophic debt:

- You lose the master key (Generalschlüssel) to your entire apartment building. Total cost for new keys and locks: €15,000+.

- A pipe bursts in your apartment, flooding the entire building. Costs: Millions in property damage.

- You accidentally step in front of a bus, causing an accident that injures five passengers. Costs: Millions in legal and medical bills.

Your Haftpflichtversicherung covers all of this for as little as €5 to €10 a month. It is the cheapest and most comprehensive protection you will ever find.

How to Choose the Right Policy

The most important features to look for are:

- Master Key Loss (Schlüsselverlust): Essential for rental apartments.

- Best Market Performance Clause: Ensures your policy automatically gets the best new terms available in the future.

- Protection Against Default: The insurer pays you if someone else injures you and they don't have liability insurance.

Special Notes for Expats:

- Pet Ownership: Dogs require a separate special liability insurance called Tierhalterhaftpflichtversicherung.

- E-Scooters: Your liability policy does not cover e-scooter accidents (which require specific insurance linked to the vehicle plate).

Summary

The "voluntary" nature of the Haftpflichtversicherung is a German myth. The real rules—set by landlords and a law requiring unlimited financial liability—make it the single most critical extra insurance you will ever buy. For the cost of one coffee a month, you protect yourself from lifelong debt, secure your housing, and show German society that you are a responsible resident.