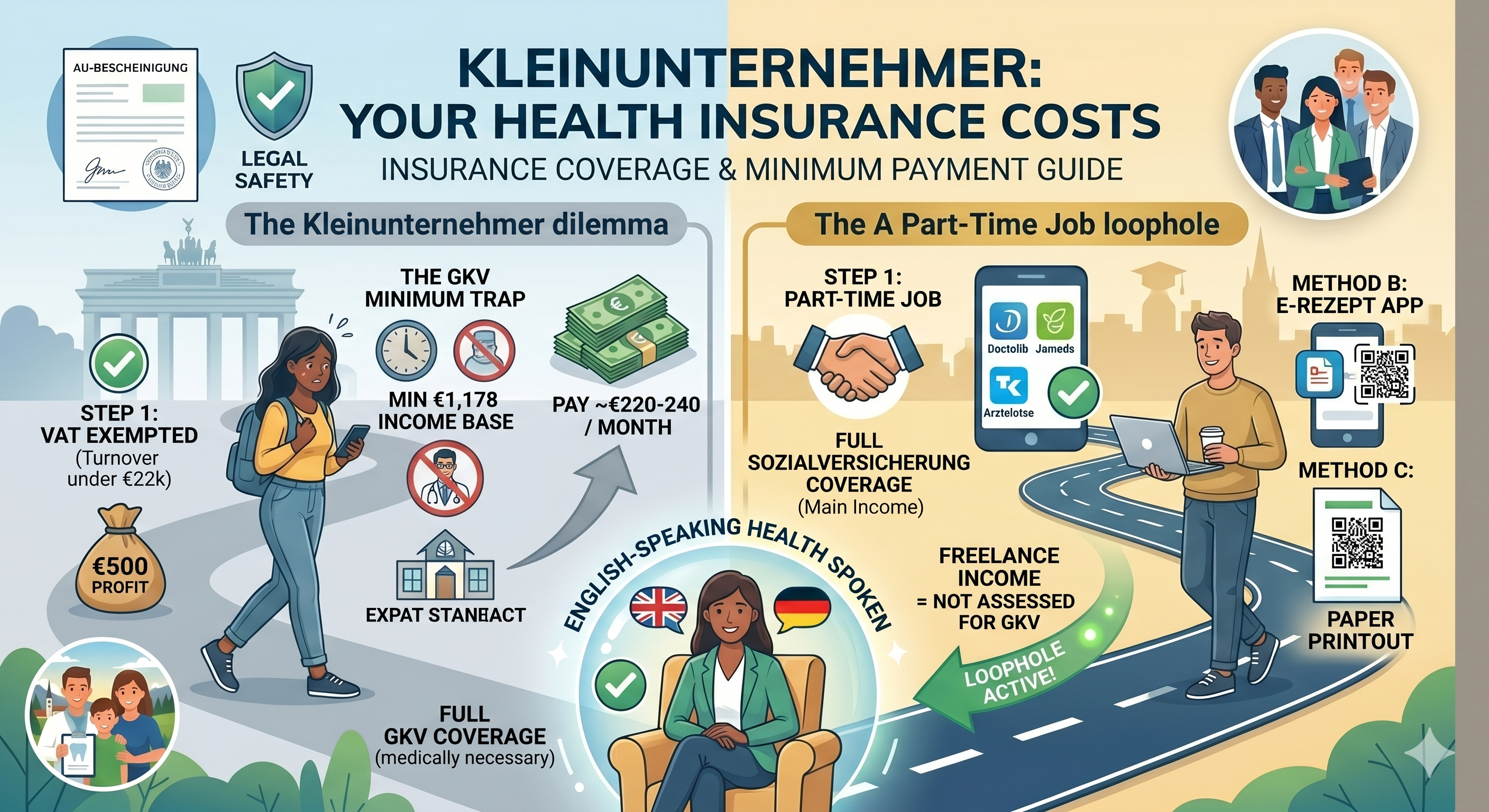

Many expats starting their freelance journey in Germany register as a Kleinunternehmer (Small Business Owner). This status applies if your turnover is under €22,000 in your first year. While it famously exempts you from charging VAT (MwSt), how does it affect your health insurance?

The Public Insurance (GKV) Minimum Premium

If you are a freelancer in the public system, your contributions are calculated based on your profit. However, there is a legal minimum income base (Mindestbemessungsgrundlage).

As of 2026, the public health insurance system assumes you make at least ~€1,178 per month, even if your actual profit as a Kleinunternehmer is only €500.

- The Minimum Cost: Because of this assumed base, the minimum you will pay for health and nursing care insurance is roughly €220 - €240 per month.

- What this means: If you are barely making money, this premium can feel incredibly high relative to your income.

Can You Pay Less?

Unfortunately, no. The €220/month mark is the absolute floor in the public system for self-employed individuals (unless you qualify for the KSK - Künstlersozialkasse).

Kleinunternehmer & A Part-Time Job

If you have a regular part-time employment job (Sozialversicherungspflichtige Beschäftigung) alongside your Kleinunternehmer business, things change completely.

- If your main income and working hours come from your part-time job, you are primarily insured through that job.

- In this scenario, your freelance income might not be taxed for health insurance at all! This is a massive loophole many expats use when starting out.