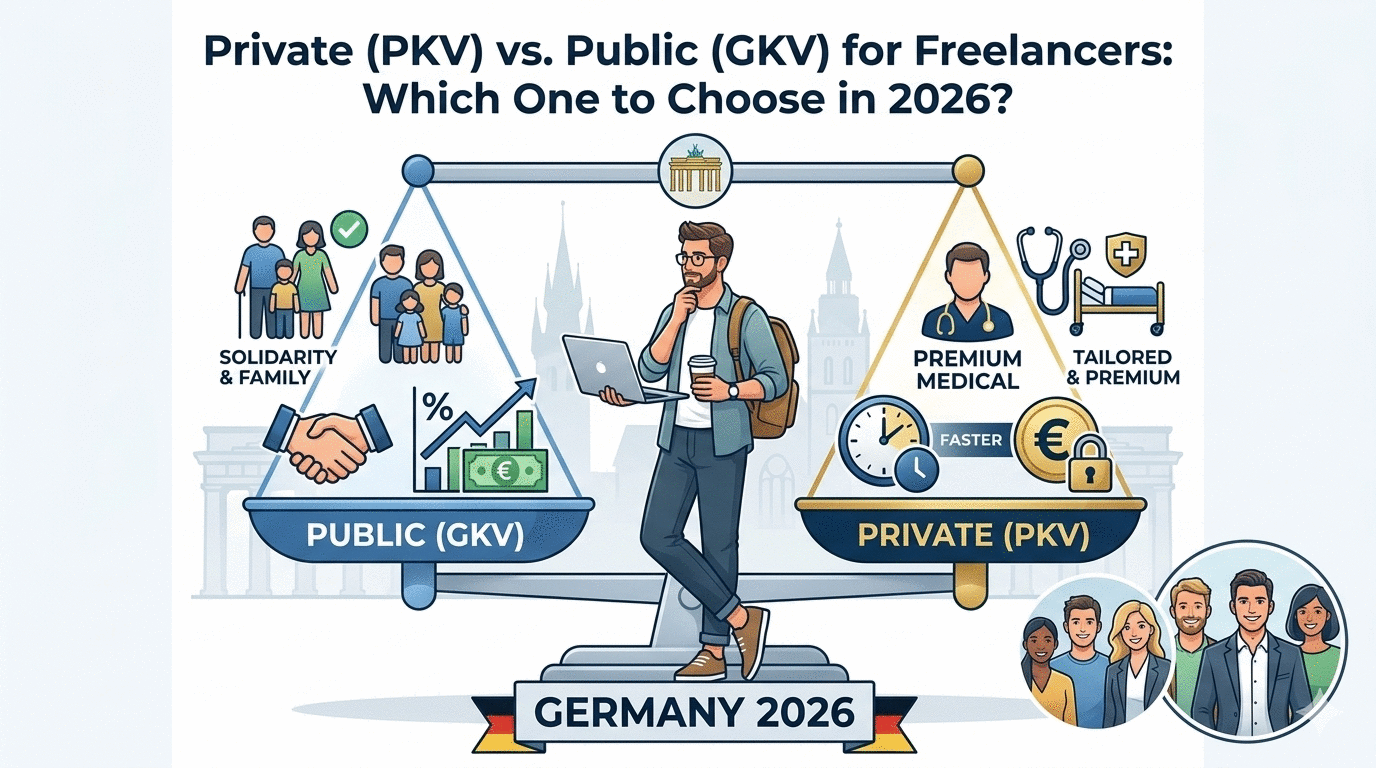

As a freelancer in Germany, you hold a "golden ticket" that most employees don't have: the right to choose your health insurance system regardless of your income. But with great freedom comes great confusion. Should you stick with the solid safety net of the Statutory Public Insurance (GKV) or opt for the tailored exclusivity of Private Insurance (PKV)? In 2026, the decision depends on more than just your monthly profit.

1. Statutory Public Insurance (GKV): The Solidarity Choice

Most expats start here. If you choose the public system as a freelancer, you are considered a "voluntary member."

- How it's calculated: You pay approximately 14.6% + an additional provider-specific fee (Zusatzbeitrag) based on your actual profit.

- The Minimum & Maximum: Even if you earn zero, there is a minimum monthly contribution (approx. €220 – €250). Conversely, there is a "cap" (Beitragsbemessungsgrenze) where your premium stops increasing even if your profit keeps growing.

- The Big Advantage: Family coverage. If you have a non-working spouse and children, they are insured for free under your plan.

2. Private Health Insurance (PKV): The Performance Choice

Private insurance in Germany is not based on your income, but on your individual risk profile.

- How it's calculated: Your premium depends on your age at entry, your health status, and the level of benefits you choose.

- The Advantage for High-Earners: If you are a young, healthy freelancer with high profits, PKV is often significantly cheaper than the public system because it doesn't scale with your income.

- Exclusive Benefits: Faster access to specialists, single-room hospital stays, and superior dental treatments that the public system simply doesn't offer.

3. The 2026 Comparison: Pros and Cons

| Feature | Public (GKV) | Private (PKV) |

|---|---|---|

| Monthly Cost | Linked to your profit | Linked to age/health |

| Family | Free for kids/spouse | Separate premium per person |

| Medical Service | Basic / Functional | Premium / Fast access |

| Old Age | Remains stable %-wise | Premiums can rise (need aging reserves) |

| Flexibility | Hard to leave once you're older | Easy to customize benefits |

4. Which one is for you?

Choose Public (GKV) if:

- You have (or plan to have) a large family.

- Your income fluctuates significantly year to year.

- You prefer a "set it and forget it" system without health exams.

Choose Private (PKV) if:

- You are a single, high-earning professional.

- You want the best possible medical treatment and priority appointments.

- You are young and want to lock in a lower rate now.

- You want a fixed cost that doesn't increase just because your business is more successful.

The "Point of No Return"

Be careful: Switching from Private back to Public is extremely difficult after the age of 55. This is a long-term decision that requires a strategic view of your life in Germany.